This blog was authored by EDF economists Aurora Barone, Luis Fernandez Intriago and Jeremy Proville.

As Congress returns to debate the future of clean energy tax incentives, sound economic analysis should drive decisions.

These incentives aren’t just climate policy; they represent strategic investments in America’s economic future, energy security, and global competitiveness. As Congress considers major changes to clean energy incentives, focusing on economic fundamentals reveals the substantial risks that come with repeal.

The Stakes

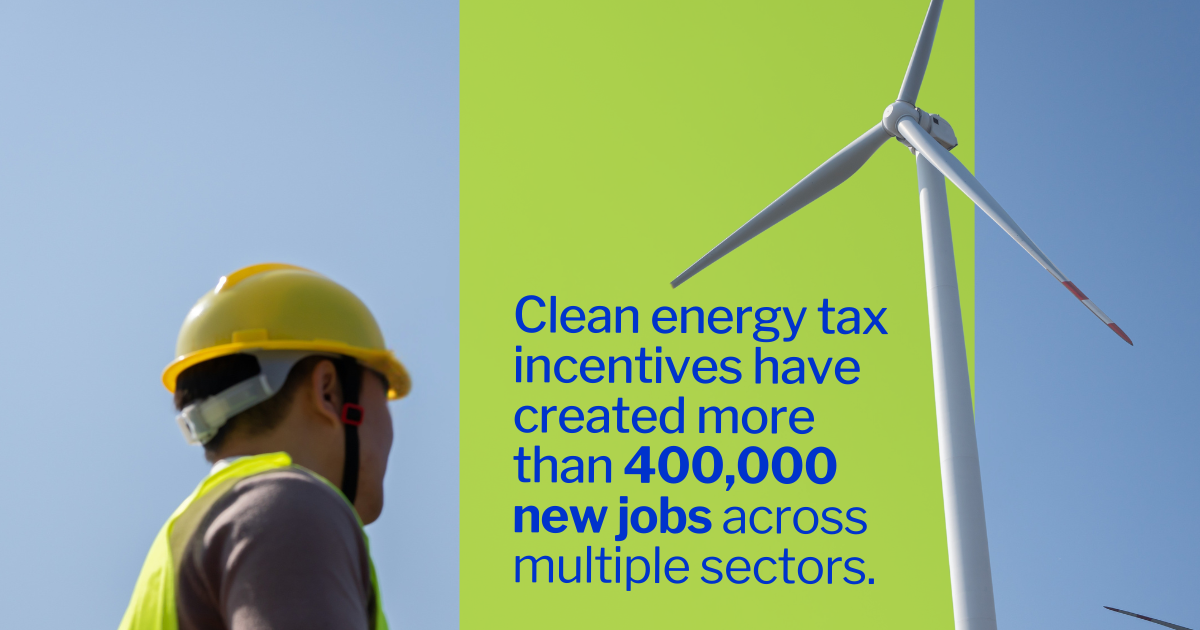

The debate over clean energy tax incentives comes at a pivotal moment for American economic competitiveness. U.S. electricity demand is surging and projected to increase 54% by 2035 and 135% by 2050, driven by new data centers, new manufacturing facilities in the US, and electrification of buildings, transportation and industry. This dramatic increase raises fundamental questions about how the US can power our growing economy affordably and reliably. Early evidence shows that clean energy incentives are delivering strong economic returns. They’ve already created more than 400,000 new jobs across multiple sectors.

Repealing them would threaten American livelihoods, energy affordability, and domestic production capabilities. According to multiple economic studies, repealing these incentives would increase consumer energy costs while undermining America’s energy independence during heightened global instability.

Employment and Investment Impacts: The Numbers

Multiple independent economic analyses demonstrate that repealing clean energy tax incentives would cause significant economic harm. This wide range of estimates reflects different modeling approaches and assumptions, but the consistent conclusion is that repeal of the clean energy provisions would significantly harm American employment and economic growth:

- Aurora Energy Research: Net loss of 97,000 clean energy jobs across 31 states (103,000 fewer clean energy jobs, only partially offset by 6,000 new fossil fuel jobs; does not include job impacts on manufacturing)

- International Council on Clean Transportation: 130,000 auto manufacturing jobs directly threatened, plus 310,000 additional indirect jobs by 2030

- Energy Innovation: Nearly 790,000 jobs lost by 2030, over 700,000 still missing by 2035

- Brattle Group: Cumulative loss of 3.8 million job-years through 2035 (averaging 345,000 jobs annually)

Clean Energy Tax Incentives as Job Creation Engines

The reason why reversing these clean energy incentives has such a sweeping impact that could eliminate so many jobs is because they take a comprehensive approach to job creation. Unlike narrow policies targeting single industries, these incentives offer broader economic signals that stimulate job creation:

- Investment and Production Tax Credits: Providing tax credits for companies that produce goods or materials in the US, drives American construction and manufacturing to create long-term operations jobs in renewable energy and clean transportation.

- Clean Energy Manufacturing Credits: Boosting domestic manufacturing of batteries, EVs, and solar panels, making us competitive within global markets.

- Direct Pay Provisions: Allowing tax-exempt entities, like municipal governments and schools, to receive direct cash payments from the IRS without having to wait until tax filing to receive the benefit. Direct pay provides more flexibility for the school or church or local government to finance the project independently.

- Domestic Content Bonuses: Boosting American manufacturing of iron, steel, and manufactured products used in clean energy projects like solar and wind farms.

- Energy Community Incentives: Targeting job creation in regions transitioning from fossil fuels.

The geographic distribution of these benefits is particularly impressive. The top 20 congressional districts account for over 100,000 operational jobs from announced projects catalyzed by these incentives. These incentives significantly impact employment in construction across diverse South, Midwest, Southwest, and Mountain West regions. Of 390 announced clean energy projects, over 60% are in Republican congressional districts.

Notably, these job figures primarily reflect announced projects and may underestimate the full employment impact. The Department of Energy’s U.S. Energy Employment Report (USEER) methodology captures a broader range of indirect and induced jobs throughout supply chains and local economies that aren’t always reflected in project announcements. This suggests the economic benefits of clean energy incentives may be even more substantial and widespread than current estimates indicate.

Public Health and Economic Savings

A crucial but often overlooked economic dimension is reduced air pollution’s substantial public health benefits. The Treasury Department projects health benefits valued at $20-49 billion annually by 2030 from clean energy tax incentives. These represent real economic savings that offset a significant portion of the program’s fiscal expenses, including avoided healthcare costs, increased productivity, and reduced mortality risk.

Energy Security and Strategic Competition

As of 2024, nearly half (42%) of U.S. electricity comes from low-carbon sources. This diversification strengthens American energy security and energy dominance – strategic advantages that would be undermined by repeal. Solar and wind generation are playing dual roles: both replacing retiring coal capacity and meeting rapidly rising electricity demand, particularly during extreme weather events that are increasingly straining the grid.

Repealing clean energy tax incentives would leave the United States more dependent on natural gas to meet rising demand, creating multiple vulnerabilities:

- Price Volatility: Natural gas prices can spike dramatically during extreme weather events, affecting consumer costs and economic stability

- Geopolitical Exposure: Greater reliance on a single fuel source increases vulnerability to global energy market disruptions

- Supply Constraints: Natural gas infrastructure requires significant lead time to develop, potentially creating bottlenecks

- Strategic Disadvantage: While global competitors like China and India rapidly build clean energy capacity, repealing incentives would cede America’s competitive position

Understanding Fiscal vs. Economic Costs

Critics often focus exclusively on fiscal costs, presenting an incomplete economic picture. The Treasury Department’s analysis distinguishes between fiscal costs (payments from the government to individuals, e.g. a government bailout or government spending on infrastructure) and true economic costs (net losses to the overall economy, e.g. costs of pandemic, natural disasters on an economy).

Multiple forecasts estimate the fiscal costs of these clean energy tax incentives:

- Credit Suisse: $800+ billion

- Brookings Institution: $780 billion through 2031

- Goldman Sachs: $1.2 trillion

- University of Pennsylvania: Just over $1 trillion (2023-2032)

However, as Treasury explains, in the context of clean energy incentives, “fiscal costs are the wrong costs to consider.” The Office of Management and Budget’s Circular A-4 recommends that transfers be excluded entirely from economic analysis or counted as both a cost to the government and a benefit to taxpayers.

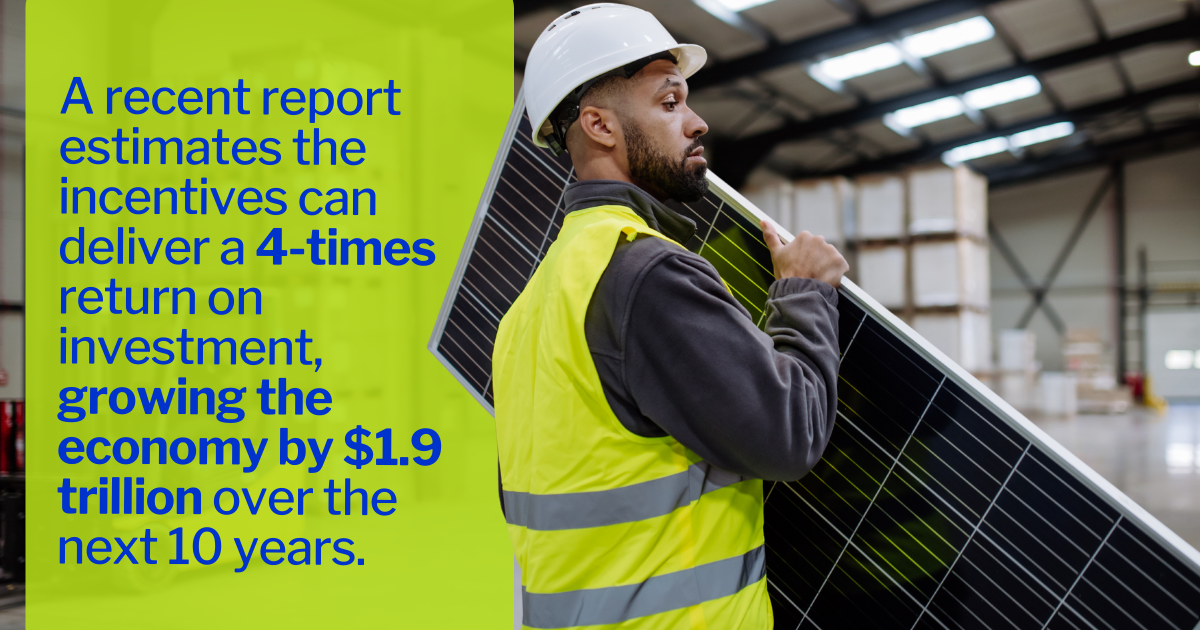

An economic analysis must account for the full value generated, including jobs, consumer savings, health improvements, and environmental benefits. A recent report estimated that the tax credits will deliver a 4x return on investment that grows the economy by $1.9 trillion over the next ten years, and further comprehensive studies will be key in better assessing impacts on American households.

Conclusion: Policy Stability Drives Economic Growth

Any subsidy can spark job growth, so the real question is: which types of jobs will last and lift communities for years to come? The ones spurred on by clean energy incentives are creating durable opportunities in manufacturing, construction, and research that far surpass job quality from sunsetting legacy energy industries with high social and environmental costs.

The economic case for preserving clean energy tax incentives is compelling across multiple dimensions:

- Employment Impact: Preserving millions of job-years across diverse regions and sectors

- Consumer Protection: Preventing $75-400 in increased annual household electricity costs that would function as a regressive tax

- Health Economics: Delivering tens of billions in annual health benefits from reduced air pollution

- Energy Security: Strengthening America’s resilience against price volatility and geopolitical tensions

- Regional Development: Driving investment to communities across the country, including those transitioning from fossil fuel economies

While more ambitious climate policies theoretically exist, the clean energy incentives are already working and have earned broad, bipartisan support. Repealing them now would introduce harmful volatility that undercuts American jobs, economic growth, investment certainty, and global competitiveness. The evidence is clear: preserving these incentives represents prudent economic policy that strengthens America’s future.