New analysis shows Arizona utilities could save Arizonans millions by joining a West-wide electricity market

Written By

Share

This blog is part of a series by EDF on the development of a regional electricity market in the West. Other blogs in the series explore the overall importance and benefit of a regional market, the impacts of market participation in Colorado and California, and opportunities unlocked via passage of California AB 825.

After decades of effort, a regional electricity market in the Western U.S. is taking shape. Recent legislation in California marked a critical step forward in a decades-long process to establish an independent, West-wide power market that will deliver cleaner, more affordable and more reliable electricity to consumers in the West. This new market could deliver real savings to Arizonans’ electricity bills. To fully realize these benefits, utilities must embrace regional cooperation.

Arizona’s largest electric utilities, including Arizona Public Service (APS), Salt River Project (SRP), and Tucson Electric Power (TEP), are all primed to join a regional “day-ahead market” within the next few years. They have two options: 1) the Extended Day-Ahead Market (EDAM), which will be governed by a new independent Regional Organization for Western Energy (ROWE) and operated by the California Independent System Operator, which is poised to be the largest and most resource-diverse market in the region; and 2) Markets+, another day-ahead electricity market that will be run by the Southwest Power Pool.

New analysis from Aurora Energy Research and EDF compares these two options and finds that APS could save its residential customers nearly $110 million annually more than projected under their current market selection if they instead went with the larger market option. For APS customers, that’s about $50 per year in savings. Additionally, if all Arizona utilities joined the larger market, they would collectively save $114.9 million per year more than the alternative market. These results underscore the significance of this decision for the utilities and their consumers in Arizona.

Why markets matter for Arizona

Arizona stands at a pivotal moment for its energy future. Last August, state utilities experienced record-breaking peak demand driven by high temperatures exceeding 110 degrees across Phoenix and Tucson. It follows a trend of electric demand exceeding summer forecasts as heatwaves become more common due to climate change.

At the same time, growing industrial demand for power, primarily from data centers, is reshaping the state’s energy landscape. If all proposed data center facilities are built, APS and Salt River Project, the state’s two largest utilities, could face up to 17,000 MW and 12,000 MW respectively in new demand by 2038, more than doubling their current peak capacity. These and other pressures are leading to significant cost increases for Arizonans; for example, last year APS proposed a rate increase of nearly 15% for residential consumers, outpacing the national consumer price index of 6.7% for electricity services.

With over 11,000 MW of installed solar capacity and projections to exceed 14,000 MW over the next five years, the state ranks among the top five nationally for solar generation. This could position Arizona as a leading exporter of cheap, clean power, when it produces more than it can use. Efficient regional structures that integrate and dispatch energy across state lines can generate new revenue while displacing more expensive power when needed.

Arizona needs solutions that can drive more efficient use of energy resources to limit cost increases wherever possible and ensure reliable electric service despite more strain on the grid. Expanding the use of markets to facilitate more trading between Arizona and its neighboring states is one such solution, and Arizona utilities are actively pursuing joining new markets to share energy resources and balance load growth. However, the choice of market matters in terms of the scope and scale of benefits both utilities and their customers can garner from trading efficiencies.

Utilities can already buy and sell power with each other via bilateral trading agreements, but markets create opportunities to optimize trading between many participants across a wider geography. In short, this benefits Arizonans by allowing their utilities to buy the cheapest power available and to sell their excess power to more customers when it’s not needed in Arizona. A wider market geography also means access to more diverse sources of power when Arizona needs its most, reducing the risk of reliability problems like brownouts at moments of grid stress.

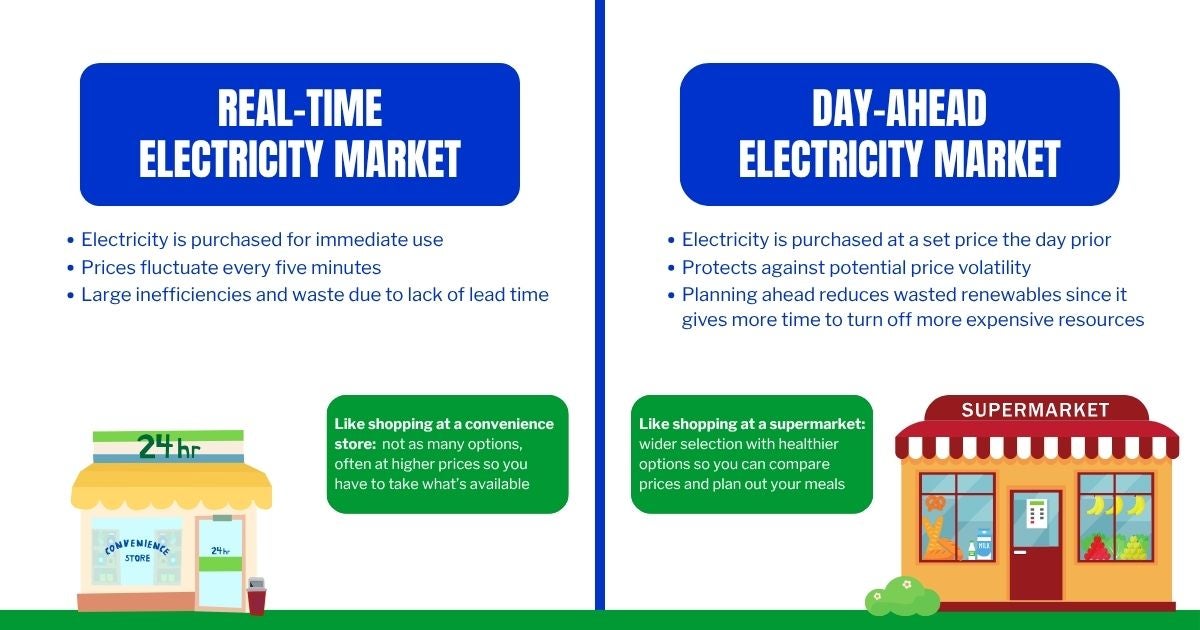

Arizona’s existing real-time market

Arizona’s utilities have already seen the benefits of regional markets through the Western Energy-Imbalance Market (WEIM), a voluntary real-time market launched in 2014 that lets utilities buy and sell power to manage near-immediate imbalances in supply and demand. By pooling their resources, WEIM participants access the cheapest energy available, which is a critical capability when localized shortages occur, like during heat waves when demand spikes. The 20 participating utilities have generated an estimated $7.82 billion in benefits, including about $128 million in savings for APS, TEP, and SRP in 2024 alone.

However, a real-time market like WEIM can only do so much — adding a day-ahead market, where utilities buy and sell power to serve forecasted needs a day in advance, would deliver even greater reliability and cost savings.

Arizona’s day-ahead market options

Since 2021, the California Independent System Operator (CAISO), which runs WEIM, has been in the process of establishing the Extended Day-Ahead Market (EDAM) to provide a day-ahead service that would benefit the West. While many utilities, including those estimated to serve nearly 50% of load in the region, have already signed onto join EDAM, several others have been reluctant to join or have actively pursued participation in an alternative market. Among those seeking an alternative include Arizona’s APS, TEP and SRP.

One main concern with EDAM has been market governance — until just a few months ago, EDAM could not be governed by an independent entity per California law. To overcome that impasse, a group of utility regulators from several Western states, including Arizona, launched the Pathways Initiative in 2023 aimed at creating a market structure that would be independent of CAISO and represent the interests of the entire region. That effort marked a major success with the adoption of AB 825 in California last September, paving the path the for creation of an independent Regional Organization for Western Energy (ROWE) — one governed by a body representing Western state interests — that will have exclusive authority over both the WEIM and EDAM, as well as future market offerings that could improve the cost and reliability of electricity throughout the West.

Over the past several years, another competing day-ahead market by the Southwest Power Pool (SPP) — called Markets+ — has taken shape. While significantly smaller and less connected than the EDAM market footprint, several Western utilities have already committed to joining including APS, TEP, and SRP.

Both EDAM and Markets+ aim to deliver cheaper, more reliable electricity, but the choice between them will shape how Arizona utilities interact with neighboring states, manage growing demand, and maintain grid reliability. For a power market, the size and footprint matter. As utilities commit to one market or the other, the benefits of regional coordination — and the risks of fragmentation — become increasingly clear.

Examining impacts of regional market options

To evaluate the potential impacts for ratepayers in Arizona of utilities’ market choices, Aurora Energy Research evaluated the impacts of APS, TEP, and SRP’s participation in two different regional market options, both of which offer day-ahead market services beginning in 2026-2027:

- Extended Day-Ahead Market (EDAM): soon to be operated by the new independent ROWE proposed via the Pathways Initiative and enabled by California Assembly Bill 825

- Markets+: operated by the Southwest Power Pool

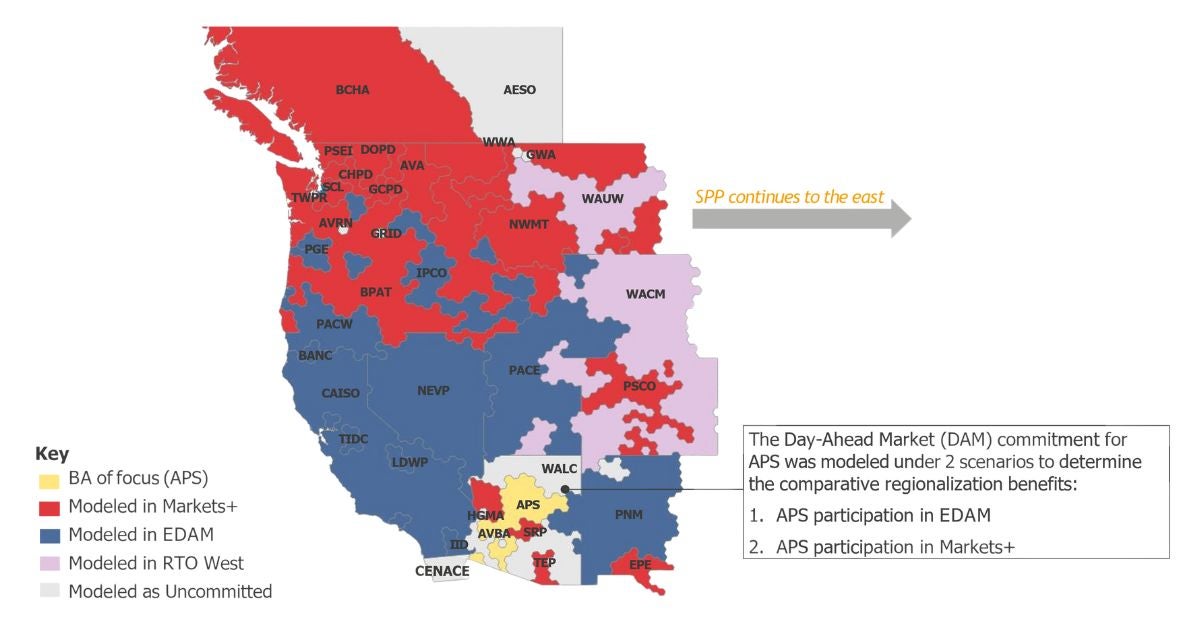

There are currently 38 balancing authorities in the West, which are the organizations in charge of managing electricity supply and demand across a geographic area, handling the dispatch of power resources to ensure the lights stay on. Currently, ten balancing authorities, have either committed or publicly signaled their intent to join EDAM — we estimate this represents 45%-50% of total electricity demand across the West.

By comparison, eight balancing authorities, which we estimate to make up about 25%- 30% of total demand in the West — and, important to this analysis, includes APS, TEP and SRP — have signaled their intention to join Markets+. Other balancing authorities in the region have not yet decided and are most likely waiting to see which market structure will yield the most benefits at the lowest cost, while a few others have opted to join SPP’s RTO West, a market option offering full RTO services. It is worth noting that the percentages cited above are for committed entities; the map below includes those balancing authorities and accounts for others that Aurora Energy Research determined likely to join one market or another.

Understanding market participants is critical because a larger marketplace, with more diverse energy resource offerings, will yield greater benefits to participants.

A bigger market yields bigger savings

To evaluate outcomes associated with participation in these two different market options, Aurora Energy Research used a production cost model to compare the revenues and costs associated with production and delivery of electricity for Arizona utilities.

Savings for APS consumers

- The modeling estimates that under a business-as-usual scenario, APS could reduce costs on average by $109.9 million annually between 2027-2040 by participating in EDAM instead of Markets+. This amounts to a total savings of over $1.5 billion over that 14-year period. If customer savings were assigned via their total energy usage, EDF estimates that over half of these savings — $57.4 million annually — would directly go to APS residential consumers, or nearly $50 per year for every single residential customer.

- The annual benefits are comparable to other independent analyses conducted for utilities in neighboring states, such as a study for Nevada’s NV Energy which found about $93.1 million in annual savings by joining EDAM compared to a cost increase of $7.3 million joining Markets+.

- These benefits are largely driven by savings in energy trading and increased revenues from the utilization of APS’s transmission system.

The full APS Report from Aurora Energy Research provides significant additional information regarding this analysis, including primary drivers of these costs savings.

Savings for TEP

- Aurora’s modeling for TEP finds that if the utility participates in EDAM instead of Markets+, its total annual costs fall by an average of ~$8.1 million (2027–2040), with benefits strengthening after the early‑2030s Springerville coal retirements.

- The net benefit is primarily driven by lower production costs (~$25 million/year) under EDAM as TEP runs fewer baseload thermal exports. This is partially offset by reduced export revenues and lower congestion and wheeling revenues relative to Markets+. Under EDAM, TEP trades less with APS and SRP, and more with PNM.

Modest costs for SRP

- Modeling for SRP shows the utility experiences slightly higher average system costs, roughly $4–10 million per year, when Arizona utilities participate in EDAM instead of Markets+, depending on the modeling scenario. This represents a system cost increase of <1–2%, meaning the effect on SRP’s total system costs is modest even though EDAM lowers Arizona‑wide costs overall.

- Under EDAM, SRP’s production costs decrease because it imports more lower‑cost renewable and thermal energy. However, these benefits are offset by higher bilateral trading costs, driven by reduced export revenues to APS, a key trading partner, and higher import costs. EDAM also increases utilization of SRP transmission ties, creating higher congestion and wheeling activity, though not enough to counterbalance the trade‑related cost increases.

Savings if all major Arizona utilities join a West-wide market

- In addition to the scenario above evaluating individual utility choice to join EDAM vs Markets+, Aurora evaluated a scenario in which all of Arizona’s balancing authority areas — including APS, SRP, TEP and WAPA Lower Colorado — all joined EDAM together. This internal Arizona coordination is consistent with what we’ve seen of the utilities’ announcements as regards Markets+ participation, and makes sense given that they have been among each other’s largest electricity trading partners.

- The analysis shows a collective savings to Arizona utilities of $114.9 million per year from joining EDAM, as compared to savings if they joined Markets+ — the largest total benefit of any scenario Aurora modeled. Like with the APS specific case, these savings are driven by improved efficiency in trading with other utilities in the EDAM footprint, and lower barriers to intrastate trading.

Considerations for future electricity markets in the West

Our analysis suggests that the larger, more resource-diverse day-ahead market offered under EDAM stands to benefit Arizonans more than available alternatives. Precisely what next steps should be taken in Arizona’s path to market participation will be determined by the utilities and state regulators.

However, the choice of market will have consequences on electricity rates, reliability and emissions for decades to come. At the very least, this analysis warrants additional consideration — and perhaps further modeling — of market choice to ensure which one is ultimately accepted by Arizona utilities is in the best interests of Arizonans.