Setting an 80 by 30 target is critical for the third RGGI program review, new EDF modeling shows

Written By

Share

As the Regional Greenhouse Gas Initiative (RGGI) undergoes its third program review, it is critical that the program scale its ambition to both meet the demands of the climate crisis and to fully capitalize on the cost-saving potential of the Inflation Reduction Act (IRA) and the Infrastructure Investment and Jobs Act (IIJA).

Ensuring ambitious reductions in carbon pollution before 2030 is key to both these objectives. A RGGI cap that aligns with at least 80% emission reductions from a 2005 baseline by 2030 (80 by 30) would reduce cumulative emissions by 182 million tons (between 2025 and 2035) relative to a straight-line trajectory to zero emissions by 2040. Reaching at least 80 by 30 in the power sector is a critical step to achieving the United States’ 2030 economy-wide commitments in line with the U.S. Nationally Determined Contribution (NDC) under the Paris Agreement, and the RGGI states should lead the way. It will also significantly increase the value of the IRA funding currently flowing into the RGGI region.

Power sector modeling commissioned by EDF demonstrates that RGGI states can achieve at least this critical level of abatement while keeping costs low. Aligning the cap trajectory with at least 80 by 30 is a “no regrets” decision that would put the RGGI region on a path consistent with nationwide climate targets. In fact, EDF’s modeling shows that RGGI could go beyond 80 by 30, implementing an 85 by 30 interim cap, achieving even greater emissions reductions at modest cost.

On top of this, near-term reductions in the power sector are crucial to enabling the effective decarbonization of other sectors. A cap aligned with at least 80 by 30 is a strong foundation on which to drive the decarbonization of transport, buildings and industry.

Near-term action is critical

As EDF has argued before, setting an 80 by 30 interim target leads to better results than simply targeting reductions either by 2035 or by 2040 — the two budget trajectories that have been modeled by the RGGI states. A program with no 2030 target will leave critical carbon emission reductions on the table at the precise moment that climate impacts are accelerating and the U.S. is sprinting to deliver on its NDC. Decreasing economywide emissions 50-52% by 2030, as the U.S. NDC requires, will necessitate rapid emissions cuts in the power sector, as electricity is a large source of low cost abatement and a necessary precondition to decarbonizing sectors like transportation and industry where electrification is key. In fact, analysis after analysis indicates that at least an 80% cut in power sector emissions is a critical linchpin for achieving our economy-wide decarbonization commitments on the 2030 timeline.

Limiting the supply of allowances in the early years incentivizes rapid reductions in carbon dioxide emissions, leading to lower cumulative emissions over the study period. CO2 can persist in the atmosphere for centuries, meaning that every year a facility continues emitting, it is contributing more to the stock of CO2 in the atmosphere. Cumulative emissions of long-lived climate pollutants like carbon dioxide, the stock of pollution built up in the atmosphere, largely govern the maximum warming — and associated impacts — we will experience. As a result, the program’s performance on a cumulative basis is a critical measure of its overall climate benefits.

RGGI states need to do two things to improve program performance

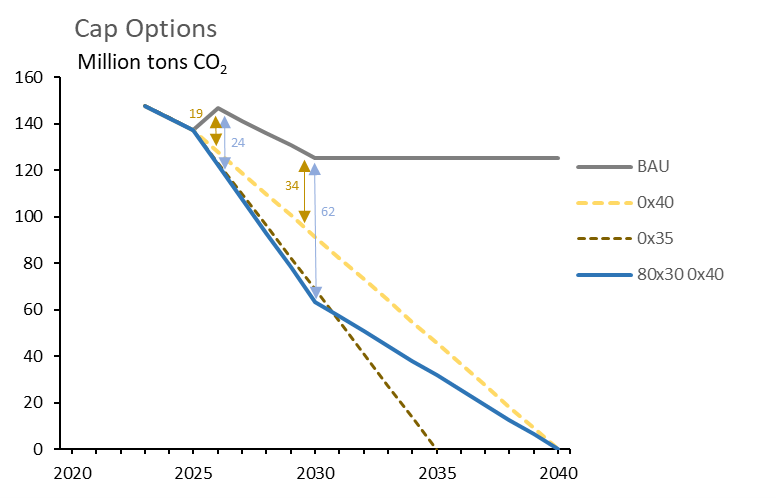

First, with 2030 fast approaching, it is critical that the RGGI states quickly and decisively finalize the program review and put a new, ambitious cap into place. The sooner such a cap is adopted, the greater its effect will be on cumulative emissions, as facilities that could be taking additional abatement measures today instead continue to produce greenhouse gases under the significantly less ambitious current cap. Every year up to 2030 that the current cap remains in place leads to an additional 19-34Mt of emissions, relative to moving to a 0x40 cap or 24-62Mt relative to an 80 by 30 cap.*

Second, the cap needs to be as ambitious as possible on the 2030 time-horizon, which will improve cumulative performance and ensure these leadership states are actually achieving power sector reductions aligned with what is necessary to hit U.S. goals under the Paris Agreement.

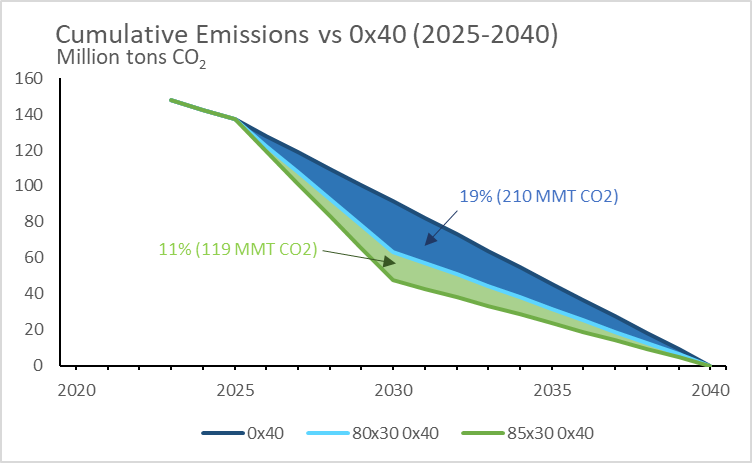

Ambitious 2030 targets drive considerable additional cumulative emissions reductions, relative to adopting a cap with a straight-line trajectory to zero.

Compared to a zero by 40 cap alone, a zero by 40 cap with an 80 by 30 interim target would yield 19% lower cumulative emissions between 2025 and 2040. Implementing an even more ambitious 85 by 30 cap would lower cumulative emissions 30% relative to a straight path to zero by 2040.

Moreover, the chart above shows that if the RGGI states adopted a cap that went through 80 by 30 on the way to zero by 40, the increased near-term reductions would mostly compensate for the longer run up to deep decarbonization, relative to the zero by 35 scenario. Securing those reductions now, while they are significantly cheaper, would help the program achieve serious environmental ambition at low cost.

These potential savings indicate the stakes of the current program review progress. Should RGGI Inc. pursue an ambitious path forward, the region could see cumulative emissions fall considerably. The certainty of a firm cap will incentivize covered entities to act quickly, while further delay in the program review process — and a less ambitious near-term (2030) trajectory — will result in slower action.

EDF’s modeling approach

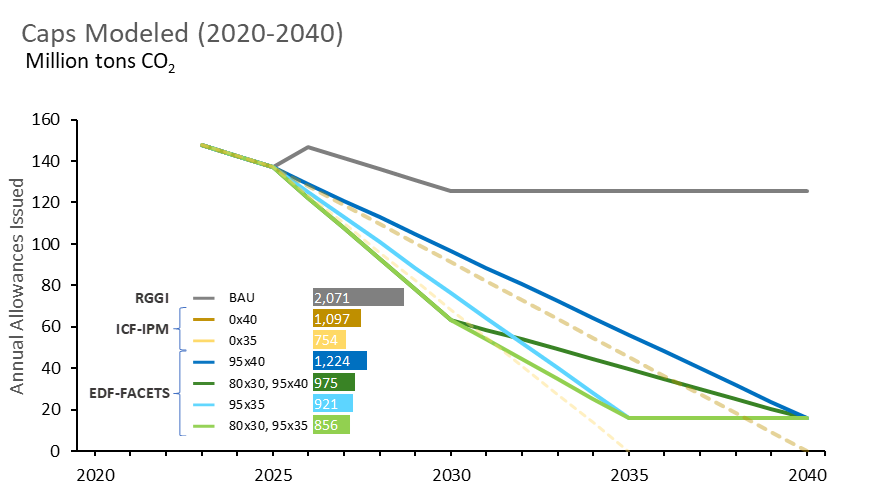

EDF’s new analysis evaluates a range of potential caps under various cost, electricity demand and policy design assumptions using FACETS, a multi-region energy system model used for power sector analysis. The model was used to demonstrate how different cap trajectories affect allowance prices, emissions, and electricity costs across a range of policy scenarios.

EDF’s modeling is intended to complement the modeling conducted on behalf of RGGI Inc. by ICF. Like ICF, EDF modeled deep decarbonization of the RGGI participants’ power sectors by 2035 and 2040 but modeled these caps both with and without an interim 80 by 30 target. EDF also tested the impact of different banking rules, leakage mitigation and the Emissions Containment Reserve (ECR) and Cost Containment Reserve (CCR).

Beyond cap and policy options scenarios, EDF tested the impact of cost assumptions for renewables and natural gas, as well as high electricity demand through a range of sensitivities.

FACETS does not solve for zero emissions, instead using a 95% emissions reduction (over 2005 levels) as an approximation of net zero.

This analysis complements ICF’s modeling using IPM, by using broadly similar assumptions and demonstrates that a more ambitious cap on the 2030 time horizon can yield very significant emissions benefits at very low cost.

High ambition at low cost

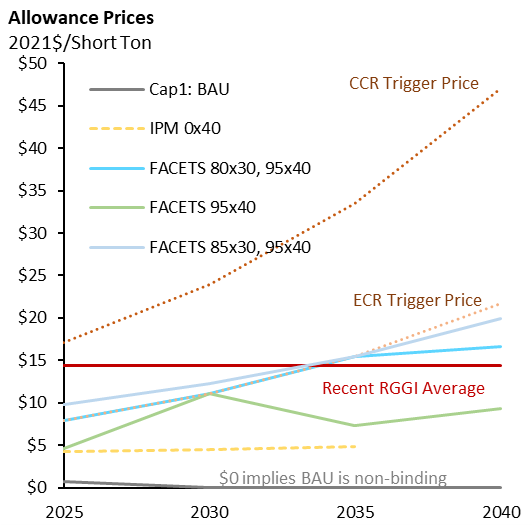

These emission reduction benefits can be achieved with a low price tag. When the cap includes an 80 by 30 interim target on the way to deep decarbonization in 2040, allowance prices remain below the recent RGGI average through 2030, and even through 2040, average allowance prices remain at or below the ECR trigger level. The RGGI system could even go beyond 80 by 30 at modest cost. Under an 85 by 30 cap, allowances prices remain near the ECR trigger price for roughly a decade and fall below the ECR trigger after 2035. Throughout the entire study period, allowance prices remain well below the CCR trigger under an 85 by 30 cap. As illustrated earlier, this cap trajectory yields considerably lower emissions, indicating that cheap abatement opportunities are readily available in the region.

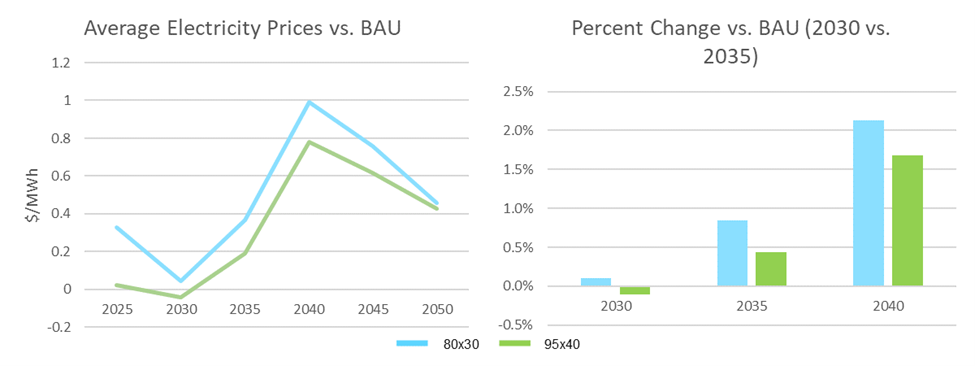

Further, the EDF analysis shows that a more ambitious cap has only a modest impact on electricity costs. The cost of delivered electricity follows a similar trajectory in scenarios with and without the 80 by 30 interim target, in spite of the emissions benefits the near-term target achieves.

Wholesale electricity costs are expected to rise over the next decade in the RGGI region, whether or not the cap is tightened. A 2040 deep decarbonization cap does not push these costs up much further and an 80 by 30 interim target does very little to drive costs up beyond that. Ultimately, gas prices and high electricity demand represent much larger upside risks to electricity prices regardless of the cap scenario. Under reference gas price and demand assumptions, an 80 by 30 cap is associated with at most a roughly 2% increase in electricity prices. To the extent that increase in wholesale prices is reflected in actual consumer bills, the impact is likely to be even smaller than 2%, as retail electricity prices include other costs and states are often deploying other strategies, including using RGGI revenue, to help lower customer bills.

The low cost of ramping up RGGI’s ambition is attributable in part to the investments made by the IRA. A November 2023 analysis from Resources for the Future modeled a nationwide 80 by 30 cap with and without the IRA, finding that inclusion of the IRA is associated allowance prices 43-66% lower than under the cap alone. While the RFF analysis considered a nationwide cap, the same fundamental dynamic is at play in the RGGI system. That is, the IRA buys down the cost of clean energy resources, easing the cost burden of electricity providers substituting away from fossil fuels.

It is the perfect moment for RGGI to take advantage of the IRA investments, leveraging the significant cost declines to lock in policy frameworks to ensure emissions abatement at significantly lower cost.

Conclusion

EDF modeling results clearly show that more ambitious caps for the RGGI system — caps that actually match the ambition necessary from the electric power sector — will not drive up costs. Enacting a cap that requires at least an 80% reduction below 2005 levels by 2030 would generate significantly greater climate change mitigation benefits without meaningfully impacting electricity prices. The RGGI states should prioritize including this interim pollution reduction goal in their third program review.

* The difference in annual emissions between cap trajectories varies from year to year, with caps beginning to diverge in 2026. The difference between the BAU cap and more ambitious caps general increases in the later years, as the BAU cap levels off after 2030 but other caps continue to decline.