This post was co-authored by Drew Stilson, Senior Analyst, U.S. Climate Policy at EDF

In an update to a previous analysis from EDF and M.J. Bradley & Associates, our latest modeling shows significant environmental benefits stemming from Pennsylvania’s proposed plan to cap power sector carbon emissions and participate in the Regional Greenhouse Gas Initiative, known as RGGI.

RGGI is a collaboration of ten northeast states that is designed to lower carbon pollution from the power sector. Many businesses, environmental groups and the public support placing a limit on carbon as a necessary and effective way to address climate pollution from electricity generation.

Pennsylvania’s power sector is the fifth largest emitter of carbon pollution in the U.S., making it one of the most significant sources of carbon emissions in the country. To address emissions from the state, Gov. Tom Wolf signed an historic executive order last year directing the state’s Department of Environmental Protection to develop a regulation that is compatible with RGGI following Wolf’s commitment to reducing Pennsylvania’s climate pollution by 26% by 2025 and 80% by mid-century, compared to 2005 levels.

In April, the Pennsylvania Department of Environmental Protection (DEP) announced a starting emissions budget of 78 million tons of carbon dioxide in 2022, with the cap declining three percent annually through 2030, in line with other RGGI states’ trajectories. To evaluate the impacts of a more protective emissions budget, EDF and M.J. Bradley & Associates updated their previous analysis using a starting budget and trajectory closely aligned with the DEP cap. This analysis looked at several different scenarios based on a range of fuel prices and policies in surrounding states and found even greater environmental benefits with the updated cap trajectory. The analysis was completed prior to availability of data related to potential impacts of the COVID-19 pandemic on carbon emissions, demand and recovery. Below we have a section describing additional analysis and considerations in a COVID-19 world.

By modeling these scenarios, we can draw useful insights about expected trends in emissions, electricity generation sources, and power sector costs based on a range of different factors. Energy models, like the one used in this analysis, are not crystal balls that predict exactly what emissions or costs will be in the future, but they provide useful insights about the directional impacts of climate policies compared to a business-as-usual (BAU) scenario with no carbon limit.

Here are some of the key takeaways from the updated analysis:

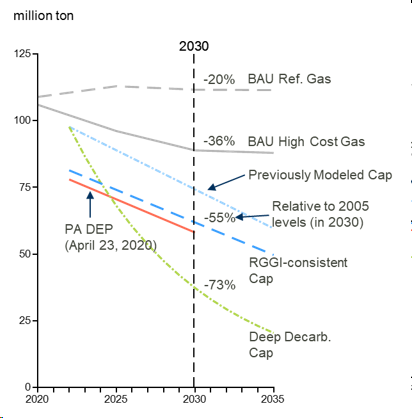

1. An updated cap reduces emissions well below Business as Usual

A more protective cap, like the one proposed by DEP, would significantly reduce power sector emissions in Pennsylvania relative to the business-as-usual scenario. The future emissions trajectory under BAU is uncertain, but by placing an enforceable cap on the power sector, Pennsylvania protects against emissions increases expected to occur by the middle of the decade due to falling natural gas prices and locks in reductions to well below BAU levels. Our analysis compared the RGGI-consistent trajectory, based on a level close to DEP’s proposed emissions cap, to a range of possible BAU scenarios and found substantial reductions compared to BAU for a range of natural gas prices.

Based on our analysis, a RGGI-consistent cap trajectory in the 12-state RGGI region, including Pennsylvania, would reduce annual climate warming emissions by 43 million tons in 2030 across the region compared to the scenario where Pennsylvania does not participate.

The results show that even while emissions may be anticipated to fall in the near-term under a business-as-usual scenario, they are expected to go back up the middle of the decade. A RGGI-consistent cap in Pennsylvania goes far beyond what the state could achieve without a limit on carbon. Importantly, participation in RGGI will bring Pennsylvania much closer to meeting its climate goals and a fully decarbonized power sector, which will not be achieved under business-as-usual.

CO2 Emissions in Pennsylvania

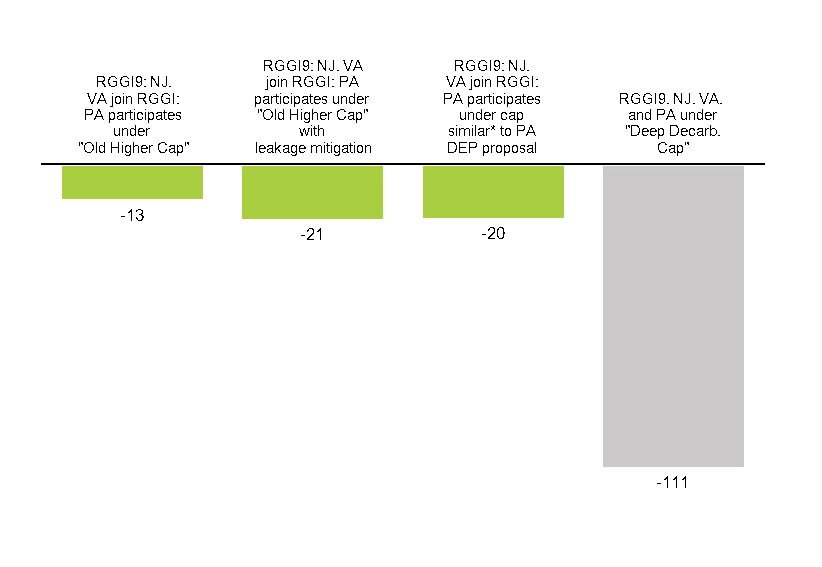

2. Pennsylvania’s carbon limit will reduce carbon pollution across the region

2. Pennsylvania’s carbon limit will reduce carbon pollution across the region

By capping their own power sector emissions, Pennsylvania’s policy will reduce annual carbon emissions in the Eastern Interconnect by roughly 20 million tons by 2030. This means that even accounting for shifts in power generation between states in the region that might result from a RGGI rule, the overall emissions from the region in total are expected to fall with the cap in place.

This result demonstrates that while some leakage – the shifting of emissions out-of-state due to increased electricity imports – may occur, it does not outweigh the benefits of the program, because overall emissions from the region are substantially lower than BAU levels. An effective leakage mitigation mechanism, like placing emissions associated with imported electricity under the cap, can achieve even greater regional reductions.

Eastern Interconnect: Reduction in CO2 Emissions Compared to BAU (million tons in 2030)

*EDF modeled a cap that is roughly 5% higher than the cap proposed by PA DEP on April 23, 2020.

3. The proposed cap provides more support for zero-emitting resources

RGGI’s cap-and-trade approach to reducing power sector emissions is technology-neutral and ensures the most cost-effective deployment of zero-emissions resources to meet the required reductions. As we noted in our previous blog post, BAU conditions would likely lead all nuclear capacity in Pennsylvania to retire by 2030. Under a more protective cap, support from the price placed on carbon emissions will result in roughly twice as much nuclear generation in 2030 compared to EDF’s previously modeled, less stringent cap.

In-state Generation Mix and Est. Exports (TWh in 2030)

*EDF modeled a cap that is roughly 5% higher than the cap proposed by PA DEP on April 23, 2020.

4. RGGI will bring jobs and economic opportunity to Pennsylvania

While this analysis did not look specifically at macroeconomic impacts or evaluate potential reinvestment portfolios for allowance proceeds, we know from experience that RGGI produces significant economic benefits to states. DEP recently released analysis that projects a net increase of 27,000 jobs in the Commonwealth from RGGI, as well as significant benefits to public health from pollution reductions.

The nature of the RGGI program keeps costs low – by allowing the price on carbon to drive reductions and allowing plants to trade emissions allowances, companies can identify and implement the most cost-effective measures to achieve emission reductions.

Pennsylvania can implement this policy while maintaining significant electricity exports. In fact, modeling results show a 65% increase in net exports in 2030 compared to 2018, as shown in the chart above. This indicates that Pennsylvania can continue to generate revenue by exporting electricity while simultaneously reducing its climate impact. Most of these exports are to other RGGI states, so the overall pollution from the region is not affected.

Other studies have shown that by driving investments in energy efficiency, RGGI has already reduced consumer energy bills, boosted the economy and produced enormous public health benefits. By encouraging cleaner methods of generating electricity, RGGI has reduced air pollution, helping save hundreds of lives, preventing thousands of asthma attacks, and saving billions of dollars in health-related economic costs. DEP’s analysis shows that the program will reduce SO2 emissions by up to 67 thousand tons and NOx emissions by up to 112 thousand tons in the state by 2030.

Electricity bill modeling by the Analysis Group found that the average residential electricity bill in RGGI states will be 35% lower in 2031 than it is today, due in part to investments in energy efficiency – an approach Pennsylvania can follow to yield benefits for its own ratepayers. EDF and M.J. Bradley & Associates’ modeling found that allowance prices are expected to remain under $10 per ton through 2030 in most scenarios, showing that even with a more stringent cap, the impact to ratepayers will be minimal.

5. Implications of the COVID-19 pandemic

A recent analysis from Rhodium Group demonstrates that the COVID-19 pandemic has impacted the transportation sector and its emissions more than the power sector, but there have been some effects on electricity generation. Demand has weakened in the power sector and emissions have accordingly declined, a trend expected to continue through the mid-2020s before reductions flatten, according to the analysis. Coal-fired generation was expected to further decline due to its lack of economic competitiveness with more cost-effective, clean sources, and COVID-19 augments this trend. However, Rhodium notes that “COVID-19 will leave a legacy of a more carbon intensive economy compared to our pre-COVID baseline without additional policy action,” because while COVID-19 does force emissions lower it reduces economic output even more, which means we are becoming more carbon intensive – emitting more pollution per unit of GDP. This demonstrates that we need policies in place to continue to drive down and ensure emissions reductions, with the added benefit that proceeds from programs like RGGI could be reinvested to help rebuild cleanly after COVID-19 and help ensure fairness for impacted workers and communities as transition continues.

Room for more ambition

EDF applauds the Pennsylvania DEP for moving forward with capping power sector emissions and for selecting a cap trajectory that ensures significant reductions below business-as-usual. Our analysis shows that the benefits of the program continue to accrue with even more ambitious caps, and an emission reduction trajectory aligned with deep decarbonization is imminently feasible for the region. A deep decarbonization trajectory that gets close to zero by 2040 with leakage mitigation mechanism in place could reduce annual emissions 111 million tons across the Eastern Interconnect by 2030. Further, a deep decarbonization trajectory brings even more solar capacity into the region’s electricity generation mix and maintains all of the state’s existing nuclear fleet (except for retirements that have already been announced). Higher allowance prices resulting from a deep decarbonization trajectory would generate more proceeds for the state to invest in clean energy, energy efficiency, and other job-creating programs. Legislation just introduced in the state legislature also underscores additional important priorities for investing proceeds, including in ratepayer protection programs and to benefit impacted fossil fuel workers and communities.

EDF commends DEP for its ambition in capping power sector emissions, and we encourage the department to move forward with the proposed RGGI rule to deliver the climate, public health and reinvestment benefits that are strongly supported by Pennsylvanians.