Climate change solutions

We deliver game-changing environmental solutions that have a real impact for people around the globe.

Medium- and heavy-duty electric vehicles are hitting the road in 2026, and we’ve collected last month’s most exciting news. In 2025, EDF delivered monthly deployment updates on the biggest zero-emission transportation stories. By the end of 2025, it was clear that momentum was sustained throughout a challenging year. This year will undoubtably see more big announcements, and we’ll be here to showcase the biggest orders and deployments of zero-emission trucks happening around the country.

April announcements from major U.S. carriers preceded the start of ACT Expo on May 4th, where major shippers and carriers, OEMs, and fleets will convene to shape what’s next in freight and commercial transportation. These announcements reflect the significance of this moment: even as regulatory signals shift, companies are continuing to invest and signal what they need to scale. The next phase will be shaped by how companies engage, and whether they use their voice and influence to help build the policy, infrastructure and market conditions they depend on to succeed. EDF works with fleets to help enable sustainability leadership and translate it into market and policy progress.

Einride to deploy 75 electric trucks for Amazon’s US freight network

Amazon is expanding their zero-emission vehicle operations by adding 75 Class 8 Einride trucks to their freight network, focusing on middle-mile transportation. Amazon has focused on their partnership with Rivian, aiming to add 100,000 Class 2b electric vans to their fleet, with around 30,000 vans deployed in 2026. The 75 heavy-duty trucks will move orders between Amazon’s fulfillment centers, sort centers, air facilities and last-mile delivery stations. Einride will support charging infrastructure across five locations.

FedEx Introduces New Electric Vehicles to its Operations in Puerto Rico

FedEx has introduced 26 electric delivery vans to its fleet in Puerto Rico, replacing older diesel vehicles and bringing the electric vehicle total to 19% of the local fleet. The deployment consists of Mercedes-Benz eSprinter vans that will operate across major cities like San Juan. FedEx continues to transition its fleet to zero-emission not only in the U.S., but across Latin America and the Caribbean to align with its global goal of achieving carbon-neutral operations by 2040 through a phased move to zero-emission delivery vehicles.

Averitt set to deploy battery-electric yard tractors

Averitt will deploy battery-powered electric yard tractors at service centers across Tennessee, supported by the state’s Medium- and Heavy-Duty Vehicles Grant Program. The company remains committed to sustainability initiatives including investments in fuel-efficient equipment, innovative technologies and initiatives designed to reduce emissions and conserve resources. These efforts are part of a strategy to operate responsibly while delivering consistent, dependable service to customers.

Now is a critical time for fleets to invest in medium- and heavy-duty electric trucks. These vehicles improve public health and help combat the climate crisis by reducing greenhouse gas emissions and air pollution. Unlike traditional diesel-powered trucks, electric trucks produce no tailpipe emissions, which significantly cuts down on health-harming pollution. At the same time, these vehicles can help fleets manage exposure to volatile fuel prices and improve long-term operating cost stability. Adoption represents a key step toward a more sustainable and resilient transportation industry.

Check back here next month to see a collection of the most exciting zero-emission vehicle announcements from May. In the meantime, check out EDF’s Electric Fleet Deployment & Commitment List to track announcements as they happen in real time, and view all April announcements.

Check out last month’s announcements here.

In advance of the 90th Texas Legislature, which convenes in January 2027, Environmental Defense Fund completed a detailed and thorough analysis of Texas Emissions Reduction Plan grants and nitrogen oxide emissions over the lifetime of the program. Using more than two decades worth of data provided by the Texas Commission on Environmental Quality, the newly released briefing paper details how TERP has transformed in recent years and provides recommendations for how the Legislature can further maximize efficiencies and increase market-driven investments — all without raising any new taxes or fees.

TERP provides financial incentives for projects that decrease emissions of NOx and other pollutants from mobile sources and non-road equipment and is administered by TCEQ. It includes 11 unique grant programs, including a number of advanced clean truck grants that provide significant funds for fleets to transition to cleaner trucks. In the most recent two-year budget cycle, TERP awarded over $412 million to fund 3,879 incentive grant projects that are estimated to result in the reduction of 6,137 tons of NOx emissions. Based on EDF analysis, this represents the second largest reduction of NOx emissions in the program’s history. TERP can do even more with more funding, and the additional funding is already available.

There is currently $2 billion in revenue collected for TERP prior to 2019 that is sitting untouched in a general revenue dedicated account. These funds were collected prior to TERP reforms five years ago and are used to help certify the state’s budget. For years, the conventional wisdom at the Texas Capitol was that the $2 billion in the general revenue dedicated GR-Dedicated TERP account was necessary to certify the state budget, and TERP can simply operate on new revenues collected each biennium. While that may have made sense years ago, it doesn’t made sense today — Texas has more than $26 billion in the Economic Stabilization Fund, better known as the “rainy day fund,” which is a state savings account that collects excess oil and gas revenues and makes them available for emergency appropriations. In fact, Texas’ economy has been so strong for so long that the Legislature has been able to create a number of new long-term infrastructure funds — including ones for water, transportation and broadband — while still maintaining record surpluses.

With Texas’ strong economic foundation, now is the time to use these dedicated TERP funds for their intended purpose.

For the 2028-29 budget, the Legislature should consider taking 20% of the balance, or $400 million, from the GR-Dedicated Account NO. 5071 and transferring it to the TERP Trust Fund No. 1201, to be used to supplement newly collected TERP revenue.

The funding increase can, and should, compliment ongoing reforms being considered for TERP. EDF has worked closely with the Legislature on a consolidation bill that would make it simpler for companies to apply for funds. For example, an entity seeking a newer regional haul truck and accompanying infrastructure would have to review application materials for as many as six different grant programs, each with their own specific requirements that open at different times of the year. For entities trying to align their budgets and timelines for vehicle and equipment replacement schedules, navigating the large number of grants can be a significant barrier to participation. A TERP consolidation bill will make it easier for companies to apply, and free up considerable agency time. Additionally, the additional dollars that would come from increasing TERP funding by $400 million would also include, by law, a percentage of funds available for the administration of the TERP program. Those funds could help cover costs of any additional full-time employees required for the increased project activity.

As elected officials and TCEQ prepare for the 90th Texas Legislature next year, the policy opportunity for TERP is tremendous. Using revenue already collected for TERP and consolidating several grant programs can boost the program without increasing taxes, revenues or fees by a single dollar — doubling the economic opportunities for companies seeking clean transportation projects, as well as emissions reductions in key areas of the state.

California regulators halted the Angeles Link hydrogen pipeline, but the need to decarbonize industrial energy use has not gone away. As the state charts next steps, it needs to develop a viable decarbonization strategy for its largest gas users: heavy industry.

A proposal aimed at hard-to-electrify industrial gas operations

In 2022, Southern California Gas Company proposed Angeles Link, a dedicated green hydrogen pipeline that would serve the Los Angeles Basin. Their goal was to deliver hydrogen to large industrial users, power plants and other customers that cannot easily electrify.

The concept centered on building new pipeline infrastructure designed specifically for hydrogen rather than trying to force it through an existing gas system that was not built to handle it safely or reliably. Purpose-built infrastructure would avoid many of the safety and material compatibility challenges associated with repurposing pipelines designed for methane transport.

SoCalGas positioned the project as a way to support regional hydrogen production and reduce emissions in hard-to-electrify sectors. At the same time, it asked regulators to approve recovering early development costs from natural gas ratepayers, raising concerns about cost allocation and financial risk.

Ratepayers should not bear the risk

After years of debate, regulators drew a clear line and denied SoCalGas’s request to recover costs for the next phase of Angeles Link, effectively putting the project on hold. The decision protects residential customers from paying for infrastructure designed primarily for large industrial users, a central concern throughout the proceeding. It also reinforces a key principle: ratepayers should not carry the risk of speculative infrastructure investments.

At the same time, the proceeding surfaced broader questions that remain unresolved. Should regulated utilities play a role in developing hydrogen infrastructure? If so, under what conditions, and who should pay? Those questions will shape California’s path forward.

Hydrogen must deliver real climate value

The decision also underscores a deeper point. Clean hydrogen could play a role in reducing greenhouse gas emissions, but only if it delivers real climate benefits. That depends on how it is produced, transported and used.

Leakage is central to that equation. Hydrogen is not a direct greenhouse gas, but it contributes to warming through atmospheric interactions. Leaks from pipelines are not a one-time issue; they could create a steady stream of emissions over time, which can erode or even negate the intended climate benefits of hydrogen use.

This puts pressure on system design. Any future hydrogen infrastructure must minimize the distance between production and end use, utilize materials that can safely contain hydrogen and meet stricter performance standards than those applied to natural gas systems. If leakage rates are too high, the system risks undoing the benefits it has promised.

Hydrogen blending is not a decarbonization solution

While the state is not moving forward with a dedicated hydrogen pipeline, it should not assume there are viable climate benefits to blending hydrogen into the existing natural gas pipeline network. That system was built for methane, and hydrogen behaves differently. Its smaller molecules can escape more easily through seals, fittings and certain pipe materials, and it can weaken metals over time, increasing the risk of leaks and failures.

Utilities already struggle to manage methane leaks, and introducing hydrogen would add unnecessary complexity, raise costs for all customers, and deliver limited benefits. Blending achieves limited greenhouse gas emissions reductions relative to its cost. As seen in the below chart, by contrast, electrification provides a more direct, cost-effective path to cut emissions across many applications, especially for residential uses. While climate action is urgent, blending is not a practical substitute for a well-designed strategy to decarbonize industrial energy use.

California still needs an industrial decarbonization strategy

The underlying challenge remains: decarbonizing large industrial gas customers. Unlike homes, many industrial processes rely on a fossil fuel to trigger chemical reactions or generate high-temperature heat that is difficult to electrify with current technologies. For these applications, hydrogen may be one of the few viable lower-carbon options. But deploying it raises important questions about cost, risk and system design.

A more targeted approach is needed. Policymakers should assign costs to the customers who directly benefit, require shareholder investment to reduce risk to ratepayers and leverage public and federal funding to support early infrastructure development.

At the same time, regulators should set strict leakage and performance standards and tie approvals to demonstrated results over time. This approach allows progress while protecting customers from unnecessary costs and ensuring hydrogen delivers meaningful emissions reductions.

This is a reset, not the end

Angeles Link will not move forward as proposed, but the need it aimed to address is real. California now has an opportunity to move forward with greater discipline and clarity.

The state should stay focused on real emissions reductions for the industrial sector, with hydrogen playing a targeted role in a broader industrial decarbonization strategy

By Alice Alpert

When we talk about clean energy, solar panels and wind turbines usually steal the spotlight. But there’s another player waiting in the wings: Enhanced Geothermal Systems. This family of technologies could provide reliable, round-the-clock power — something renewables like wind and solar can’t always guarantee. Recently, EDF convened a group of academic and government researchers, industry and non-profit actors to examine challenges to scaling EGS sustainably and how to take action on them. We released a workshop report with more detail but here’s what you need to know.

Earth energy is always on

Geothermal energy brings heat from inside the earth up to the surface for electricity or heat. Conventional geothermal power has been in use for nearly 100 years and makes use of natural fluid systems (think hot springs). EGS takes this idea further by creating fluid “plumbing” systems in places where they don’t exist naturally. Using advanced drilling techniques borrowed from the oil and gas industry — like directional drilling and hydraulic stimulation — EGS can unlock heat from deep, hot rock formations. It could also be used to store energy and doesn’t need a lot of space

The potential is huge. According to the U.S. Department of Energy, EGS could supply up to 90 gigawatts of power by 2050 — enough to power millions of homes and support U.S. datacenters’ booming energy demand.

Getting geothermal right, now

While conventional geothermal systems are mostly in the mountain west, EGS could potentially be deployed outside that region to support the electricity needs of large populations and industrial areas. And while investments in EGS have historically been low, private investment and public research continue to rise.

Despite its promise as a clean, always-on energy source, EGS faces significant challenges before it can play a role to meet U.S. electricity needs. Now is a critical time to get our ducks in a row. A multi-pronged approach for sustainable large-scale deployment is necessary to avoid bottlenecks or impacts that could affect the industry’s future.

Prong 1: Prove effectiveness

Prong 2: Develop and use guardrails.

Luckily, they are closely connected, and if actors work smart, we can make progress on both paths faster than one alone.

Showing results

Projects are expensive upfront, and investors want proof they’ll pay off. While the earth’s heat itself is fairly well understood, there is more work to do to know whether a given well and system will be able to bring heat up to the surface efficiently:

Build some guardrails

Before any new technology is deployed it needs to be safe. This means having operational and regulatory guardrails to make ensure that geothermal development is sustainable — ecologically and socially — and to communicate safe operations to communities and regulators.

Treating these challenges together can unlock the wider puzzle and accelerate the development of sustainable EGS. To EDF that means:

For example, research to characterize the subsurface could also contribute to developing advanced seismic protocols. And because injected fluid affects earthquakes, combining reporting for water use and fluid injection volumes could also improve seismic protocols. Besides, showing investors that the technology is safe and acceptable to the public is necessary for further investment. Many of these efforts are occurring, but not necessarily in a way that maximizes efficiency and ensures that guardrails are in place before deployment.

EGS is a practical solution to one of our biggest energy challenges: how to keep the lights on without burning fossil fuels. Scaling it up sustainably will take collaboration among scientists, industry, regulators, and communities. But if we get it right, EGS could become a cornerstone of the clean energy transition.

By Elizabeth Sturcken & Marissa Nixon

A new model of leadership is developing across the freight sector. Industry leaders are moving decisively and setting a new standard of efficiency through sustainability initiatives, while others risk falling behind. The transition to zero-emission transportation is no longer just an environmental consideration — it is quickly becoming a defining factor in operational performance and competitive positioning.

A new report from Environmental Defense Fund is showcasing where leadership is taking shape across top companies, and where quiet competition is underway. The report, Four actions fleets must take to be sustainability leaders today: Benchmarking the transition to zero-emission fleets, summarizes analysis of public reports and practices among the top 100 U.S. fleets. The report demonstrates how top fleets are thinking about sustainability, and how they plan to turn ambition into action.

Fuel cost volatility is a significant business risk. Diesel, already one of the largest components of fleets’ operating expenses, has recently exceeded $5 per gallon nationally, underscoring how rapidly energy costs can shift. For companies managing large transportation networks, these price swings create real business risks, leaving freight operators exposed to external market forces and volatility. Fuel costs affect operating margins, supply chain planning and long-term investment decisions.

Sustainability is no longer separate from financial performance. Price swings affect operating margins, supply chain planning and long-term investment decisions. Transitioning to zero-emission technologies, such as electrification, offers a path to reduce fuel cost volatility, improve energy efficiency and stabilize long-term operating expenses.

EDF’s Four Actions for Fleet Leadership provides a practical framework for turning transportation sustainability into operational practice. Analysis in the report shows that leadership is not defined by any single action, but how companies align commitments, planning, deployment and industry engagement to reinforce progress and enable long-term success.

The report also highlights examples of how leading fleets are approaching this transition. For example, of the 100 companies reviewed, 60 have publicly stated transportation-related sustainability goals and 26 have committed to transitioning to zero-emission fleets or broader net-zero operations. Most companies with stated goals include timelines and interim milestones, though fewer provide detailed transition plans or deployment strategies.

These findings suggest that while progress is underway, fleets have an opportunity to strengthen execution and reinforce progress across all four leadership areas. Here, leadership is not defined by any single initiative, but by how effectively organizations align commitments, strategic planning, deployment and industry engagement to drive measurable progress.

This report highlights companies, including NFI, PepsiCo and US Foods, that are demonstrating this approach in practice by pairing long-term goals with deployment milestones, operational pilots, or supplier engagement strategies to advance transportation sustainability.“Sustainability covers more than just emissions reduction; it also includes lowering freight costs and increasing efficiency,” shares Mike Roeth, Executive Director at NACFE.

“The companies making the most progress are those connecting real-world action with longer-term planning to build more efficient and sustainable operations over time. Analyses like this help identify what leading fleets are doing differently and where the industry is headed.”

EDF’s latest report highlights where fleets are making meaningful progress, and where greater ambition is needed. For fleet operators and corporate leaders, this is an opportunity to understand how peers are navigating this transition, assess how current efforts align with emerging best practices and identify where to go further.

Amid ongoing pressure to improve cost efficiency and manage energy risk, leading companies are prioritizing transportation sustainability as a core business priority. Expectations from customers, investors, and employees are reinforcing the need for credible net-zero and zero-emission transportation strategies. Companies that align ambition with execution will be well positioned to mitigate volatility, enhance operational performance, and remain competitive as market dynamics and policy landscapes continue to evolve.

Read the full report to explore the data, see how your company compares, and identify the next steps to strengthen your fleet strategy.

By Richard Kiplagat and Angela Churie Kallhauge, this article originally appeared in The Petroleum Economist.

As global gas markets tightened in March, a tanker carrying LNG from Nigeria to France abruptly changed course towards Asia. The diversion was a small but telling signal of a larger reality: supply is constrained, competition is intensifying and every available cargo is being pulled towards the highest bidder.

At the same time, vast volumes of African gas are going to waste.

Methane that is routinely leaked, flared or vented into the atmosphere across the continent is both wasteful and damaging because methane is a powerful climate pollutant. But methane emissions are also a market failure. Unlike carbon dioxide, methane is not a useless energy byproduct—it is the product. Every tonne emitted is energy that could be used domestically or sold abroad as natural gas.

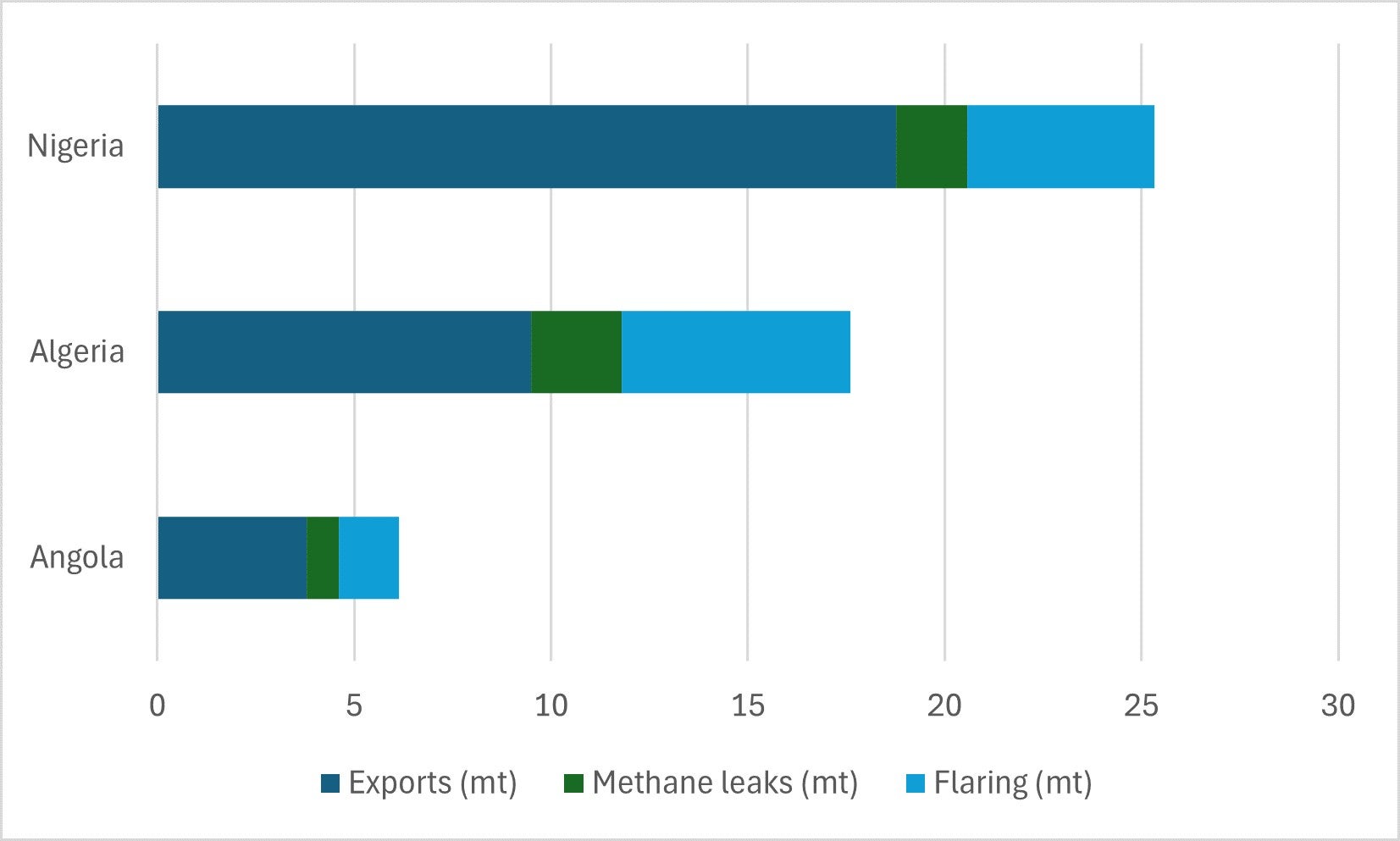

21bcm/yr – Estimated gas lost through flaring and leakage in Algeria, Libya and Egypt

At a moment of global disruption, that distinction matters. The war in the Middle East has disrupted roughly 20% of global oil and gas flows, tightening LNG supply chains and pushing prices higher. Yet this same moment presents a clear opportunity. By reducing methane emissions and gas flaring, African producers can increase supply, generate revenue and strengthen energy security without waiting years for new projects to come online.

The scale of the opportunity is substantial. According to the IEA, Africa’s energy sector emitted an estimated 17mt of methane in 2025. Every cubic metre released into the atmosphere is gas that could otherwise power homes, support industry or be exported at a premium in today’s market, leveraging Africa’s underutilised gas export capacity.

The continent can export nearly 80mt/yr of LNG, yet many facilities operate well below capacity due to upstream supply constraints. In Algeria, LNG exports in 2025 reached just 9.5mt, according to the Middle East Economic Survey, less than half of its installed capacity of 25.3mt/yr, as per Group of Liquefied Natural Gas Importers data. Even in Nigeria, where LNG facilities run closer to full capacity, methane leaks and infrastructure challenges continue to limit supply.

Capturing this gas offers a rare alignment of economic, energy and climate priorities. In North Africa alone, Algeria, Libya and Egypt lose an estimated 21bcm/yr of gas through flaring and leakage, according to calculations by Capterio. This is equivalent to around 14% of their production and up to $6b in lost annual revenue. Much of this waste can be addressed using proven technologies, often at low or even negative cost once the value of captured gas is considered.

There are already examples of progress. Angola LNG has shown that gas that would otherwise be flared can be captured and commercialised at scale. In Algeria, flare gas recovery projects and partnerships with international operators are beginning to unlock similar value. Nigeria LNG has achieved high standards of methane measurement and reporting, demonstrating what is possible across a broader system.

This shift in attitudes towards methane is being reinforced by the world’s largest gas buyers. The EU’s Methane Regulation will introduce stricter requirements on measurement and reporting, with compliance expected in the next few years. At the same time, major LNG buyers, including Japan and South Korea, are backing initiatives that favour suppliers able to demonstrate credible methane reductions.

For African exporters, this is both a risk and an opportunity. Those who act early can secure access to premium markets and strengthen long-term demand. Those that do not risk being sidelined as emissions performance becomes a differentiator.

Importantly, African governments and NOCs are not starting from zero. Many are already engaged in initiatives such as the Oil and Gas Methane Partnership 2.0, which provides a framework for measuring and managing emissions. Others have committed to ending routine flaring and reducing methane under international pledges.

The challenge now is execution—which means focusing on practical steps that can deliver results quickly. Identifying high-emission assets, deploying leak detection and repair, investing in flare gas recovery and strengthening infrastructure to keep gas in the system. It also means mobilising financing, which is increasingly accessible as better data reduces risk and improves project bankability.

International partners and technical experts are ready to support these efforts. But leadership will need to come from within.

At a time when global supply is tight and prices are elevated, the value of every molecule of gas has increased. For Africa, the methane opportunity is immediate. The gas is already there, so the question is whether it will be captured or continue to slip away.

Richard Kiplagat is a senior stakeholder relations adviser to businesses, philanthropies and government leaders, specialising in sustainable development, infrastructure, and energy. He advises a portfolio of companies that have collectively invested over $5b in Africa and was a co-facilitator of the initial strategy workshops that led to the formulation of the African Union’s Agenda 2063. As chair of the African Hydrogen Partnership Advocacy Taskforce at Africa Practice, Richard is responsible for leading and coordinating a team of global and African green hydrogen industry players, engaging with policymakers and the private sector to create an environment that accelerates investment in green hydrogen.

Angela Churie Kallhauge is executive vice-president of impact at the Environmental Defense Fund, and is based in Washington, DC. A climate and energy policy expert, she joined EDF from the World Bank, where she led the Secretariat of the Carbon Pricing Leadership Coalition for five years. She previously spent 14 years at the Swedish Energy Agency working on carbon markets, climate policy and development, including serving as the EU’s lead negotiator on adaptation under the UNFCCC and representing Sweden on the Adaptation Fund Board.

{kind=link}

{kind=link}